It’s no secret, the Coronavirus pandemic has severely affected employment, causing nearly 40 million Americans to lose their jobs, work fewer hours or become furloughed. For that reason, it’s disrupted retirement plans for a lot of people.

There are 4 common issues pre-retirees are now having to deal with. When finding a financial advisor for retirement, it’s important to discuss each scenario.

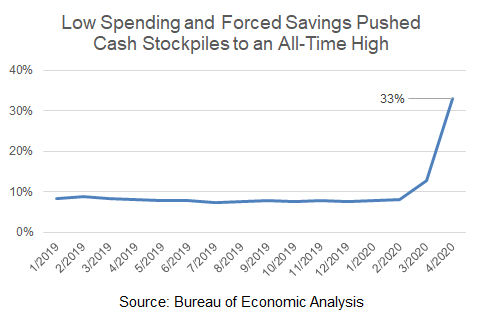

Cash Flow has Fallen Off a Cliff

The millions of job losses have detoured the budget and cash flow for many families. The income effect states that as an individual’s income increases, his or her spending will follow. The opposite is also true. The millions of lost jobs have created widespread disruptions in income, and the economic shutdown has put a hard stop on spending over the past few months.

The savings rate skyrocketed to a record 33 percent in April, indicating profound economic uncertainty. Though saving is generally a good thing, “forced saving” chokes the growth of the U.S. economy. Spending is the primary engine of the economy, so unexpected drops in spending cause lower revenue for corporations, leading to even more layoffs.

For a historical perspective, the last time the U.S. economy reached a record-high saving rate was 1975, reaching 13 percent at the tail-end of a two-year recession. At this time, simply finding financial stability is top-of-mind during this pandemic-ravaged economy.

What to Do: Revisit Your Budget and Work to Generate Cash Flow

Though easier said than done, one of your first orders of business is to get your budget back on track and to begin rebuilding your cash flow. Give your budget another look and try to devote the bulk of your spending to essentials at this time.

If you are struggling to make ends meet, see if there are any benefits from the Coronavirus Aid, Relief and Economic Security Act that you qualify for. If you can, seek opportunities to generate cash flow.

If you’re fortunate enough to have discretionary income after all of your essentials and insurance payments have been covered, use the extra funds to begin patching up parts of your finances that are not in order, such as debt payments, depleted personal and retirement savings, or business costs.

Relying on Debt

The aforementioned crash in cash flow has also forced Americans to fall back on debt to cover expenses. While useful, debt vehicles are only temporary solutions and can cause more problems in the future – especially for retirement plans.

The number of Americans carrying a credit card balance increased 43 percent from March to April. It’s understandable why people are pushed to use their credit card, considering this year’s job losses and tepid government stimulus. However, if left unchecked going forward, too much bad debt unexpectedly can push your retirement date further away. It’s important to limit the damage to your retirement plan.

What to Do: Use a Debt-Paydown Strategy Like the Snowball or Avalanche Method

There are a few strategies that are effective against bad debt. One option is the snowball method. In this strategy, you prioritize your debts based on balance amount and pay them off in order from smallest to largest. To do this, pay the minimum balance of all of your debts and focus any extra money on your smallest debt balance. Once it’s been paid off, move to the next-smallest debt balance, and so on. This can help you build confidence and gain momentum for each balance.

The avalanche method devotes your payoff efforts to debt with the highest interest rate. After paying the minimum payment for all of your debts, focus your extra money on the account with the highest interest rate. High-interest balances erode your finances the most because of their heavy interest loads, so eliminating these accounts first will save you in the long-term.

Reduced Retirement Savings

Dipping into retirement accounts is seen as a near-cardinal sin in most situations. Unfortunately, the current conditions have made heavy reliance on any savings a necessity for many people.

More than 25 percent of Americans have made retirement account withdrawals due to a Coronavirus-related job change.

Even though the economy is reopening, the economic data reveals that many still have to borrow from the future to overcome the short- and medium-term effects of the pandemic. Fixing these financial problems on an individual level will take some added effort.

What to Do: Replenish Your Retirement Accounts in Small Increments

Like credit card debt, it’s understandable if you’ve needed to take a retirement distribution to cover expenses. But if you’re working, it’s still important to rebuild your retirement balances, especially if you’re closer to retirement than not. The simplest way to maintain or restart the habit of saving for retirement is to make any retirement contributions that you can.

Throw any amount you can at your retirement account, even if it’s only $20 a month. You’re still contributing to your retirement plan, giving yourself a chance to invest and making positive steps forward overall.

Finding a financial advisor for retirement is crucial and can help you better understand your options. For example, if you’re deciding between a retirement account contribution or a higher payment toward bad debt, your financial advisor can offer advice based on your situation and will be a great resource.

Taking Care of Children, Unexpectedly

There are a number of new, unexpected expenses from COVID-19. One of the more recent financial surprises for parents is taking care of adult children. Since the pandemic, many younger adults have moved back in with their parents to stay safe and save money.

Though living with your loved ones can have a number of much-needed emotional benefits, there are still financial ramifications that affect your retirement plan. On average, it costs a parent nearly $6,000 per year to house adult children, cutting into paying off debt, future retirement savings, healthcare coverage and more.

This number can be even higher depending on your location, lifestyle and career situation. (For what you can expect in the Carolinas, download this free resource.) As important as loved ones are, you may need to find a financially suitable solution to having your children live with you.

What to Do: Come Up with a Financially Efficient Plan for Your New Living Situation

There may be a way you can live with your children and minimize your financial burden. If your child is working, consider charging an extremely modest rent or sharing the cost of smaller expenses like groceries or utilities.

These kinds of agreements can encourage financial respect between you and your children and can reduce their financial footprint on your retirement plans. Paying rent will also keep them motivated to generate income and keep their spending modest as well.

If your child isn’t working, it can still be helpful to have a money conversation, so your child knows to think about your financial needs as well as theirs.

Don’t Forget About Your Financial Advisor

It’s extremely important that you work closely with your financial advisor at this time. (If you’re working on finding a financial advisor for retirement, give Global View a test drive to see if we’re a good fit.) The current pandemic exemplifies that expert guidance is needed now more than ever. Whether you’re repairing the financial damage caused by the Coronavirus or simply giving your portfolio a tune-up, your financial advisor will complete the heavy-lifting to keep your retirement plan on track.