Quarterly Newsletter to Public Q2 2015

July 31, 2015

“It’s not stress that kills us. It’s our reaction to it.”

Dr. Hans Sely, Austrian scientist and father of the field of stress research who introduced the word stress into many European languages.

Executive Summary

We know that human beings are their own worst enemy when it comes to investing. This is demonstrated of late by a continued preference for investors to chase returns in US market capitalization weighted indexes and ETFs when the opportunity set favors a global perspective.

- In June we went to New York City to visit managers. We met with Charles de Vaulx to learn more about his approach for gaining superior risk adjusted returns. Charles worked alongside the legendary Jean Marie Eveillard at First Eagle since 1985.

- At the Pimco ecular Forum we gained much additional insight into Research Affiliates fundamental indexing strategies and learned how to implement this given the investment opportunity set. We were particularly impressed that Pimco has run a US strategy since 2005 that has added 4% excess return versus its index with substantially lower risk.

- While we continue to believe there is nearly always a better way to invest than in a market capitalization weighted index, we believe fundamental indexing is a sound way to access international markets and even US markets as appropriate.

Our Job – To Help You Take the Appropriate Risk for the Opportunity Set

In our last several newsletters we addressed the key problem investors face, specifically that they predictably take more risk to avoid a loss than to make a gain thus may be their own worst enemy. This is especially important in a world where nearly all of the returns in the last three years occurred in one market, the United States. Investors love to buy what has worked and now what has worked (over the last several years) are US market capitalization based indexes. Since we know investors chase performance it is hardly a stretch to believe they might be doing it again.

Click here for the Q1 Newsletter

While it is always impossible to predict the short-term, International markets have outperformed the US thus far this year. Through the end of June, International Developed markets were up 5.5% and emerging markets were up 3.0% while the US S&P 500 was only up 1.2%. While there has been substantially volatility primarily due to worries as China transitions from an investment driven to a consumer driven economy, valuations remain substantially better overseas. Therefore we feel it continues to be prudent to have a substantial allocation overseas especially in developed markets but also to emerging markets to some extent. At the same time we need to be aware that although emerging markets are very cheap the problems in China may be worse than many believe causing more short-term pain and keeping commodity prices lower for some time. We need to keep this in mind as we allocate assets to emerging markets and acknowledge the high short-term volatility this entails.

June Visit with Managers

In June we had the opportunity to meet with Charles de Vaulx at International Value Advisors in their office after attending the Pimco Secular Forum and meeting some of the team implementing Research Affiliates fundamental indexing strategy at Pimco.

Charles de Vaulx, International Value Advisors (IVA)

“If you are rich, the most important thing is to stay rich.” Charles de Vaulx

As our clients well know, Charles de Vaulx was an analyst and later Portfolio Manager working alongside legendary value investor Jean Marie Eveillard at First Eagle since 1985. We admire Charles and his colleagues at IVA because they took a very difficult action to close their funds. This was clearly in their clients’ interests before their own interests. They could have chosen to keep the funds open and collect higher fees. Instead they closed their funds to new investors because they felt they could better manage risk and returns at a lower asset level.

We had the opportunity to meet with Charles for about an hour and ask him questions. Charles joined First Eagle as an intern in 1985 and came back as an analyst in 1987. He is proud of his experience working with Jean Marie at First Eagle and their ability to generate positive returns in 2000, 2001, and 2002. He has learned over the years that superior risk and return depends on security selection. Companies that have a strong, enduring, competitive advantage (moat) and sell for a reasonable price are safer and cheaper than companies that do not have a moat. Figuring out whether a company has a moat requires a lot of homework. No one always gets it right. Warren Buffet bought Tesco, for example, and later sold it for a lower price. IVA did not make this mistake.

Charles recognizes that risk is often asymmetrical. Losing money can be permanent. Once you have it you want to keep it. In a world where valuations are normal only in the context of the equity risk premium, or low real interest rates, one must question what would happen to those assets if real rates rose or didn’t stay low forever. Moreover, Charles is a big believer in 20-30 year credit cycles. Given that we experienced a positive credit cycle that may have ended in 2007, it is possible we are in another negative credit cycle.

He mentioned the Blaise Pascal quote “does God exist?” The premise of this argument is that since there is a chance that God exists one should act as if he does because the risk is asymmetric, i.e. if you are wrong you suffer eternal punishment. To make an analogy, investors should understand that there is a chance that there will be a negative outcome and invest accordingly. This is especially true for investors with the most to lose.

While Charles believes profit margins in the US are stretched, he is a pragmatic investor and does not subscribe to the thematic investing approach at GMO or other firms. He believes this is an approach that is excellent in theory but does not work in reality because the world is always changing. Companies that can command higher profit margins into the future are worth more than companies that cannot.

Charles is a huge believer in the force of capitalism. Now is the best time in the history of the world to be a capitalist. He does not foresee a market crash and believes much of the global economy is mending. However, he will hold cash in the face of higher valuations for the quality companies IVA favors and not be tempted to overpay for companies simply because rates are low.

Pimco Secular Forum and Fundamental indexing

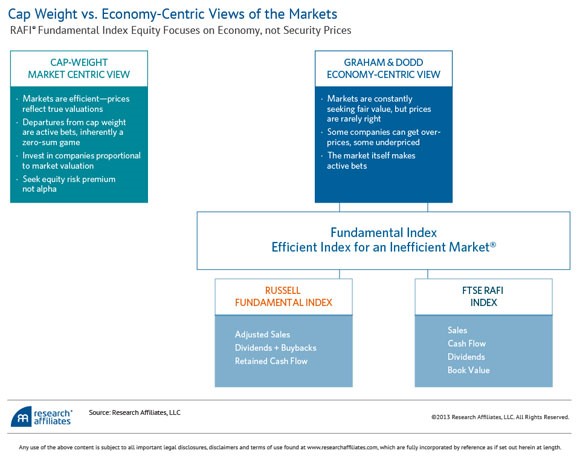

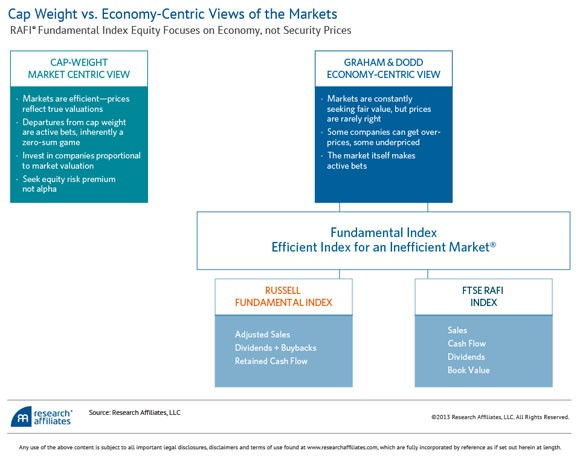

In our continual search for a low-cost way to invest we began investigating Research Affiliates fundamental indexes last year. These indexes rely on the economic footprint of companies instead of their price. The main problem with traditional indexes is that they overweight companies that are the most expensive and underweight companies that are the cheapest because they are weighted by their total size or price. Investors in these indexes believe markets are efficient and that it is futile to try to “beat the market.” Investors in these indexes must believe Warren Buffet and Jean Marie Eveillard are anomalies.

We found it very insightful that one does not have to be a stock picker to “beat the market.” In fact an extremely naive equal weighting approach has historically produced returns about 2% better than the market. The question is: is there some formulaic approach to fundamental investing that might result in better returns, i.e. can we remove “stock pickers” from the equation?

Research Affiliates studied this issue with the premise that an economic weight instead of a market price weight should result in superior results. Instead of weighting stocks by price, they weight them by their economic fundamentals, specifically: sales, cash flow, dividends and book value. The graphic below demonstrates this approach.

As one might expect, these fundamental indexes have resulted in superior returns than the market capitalization weighted indexes everyone loves. However, on another important metric to us they fell short. The indexes exhibited similar downside risk to market capitalization indexes.

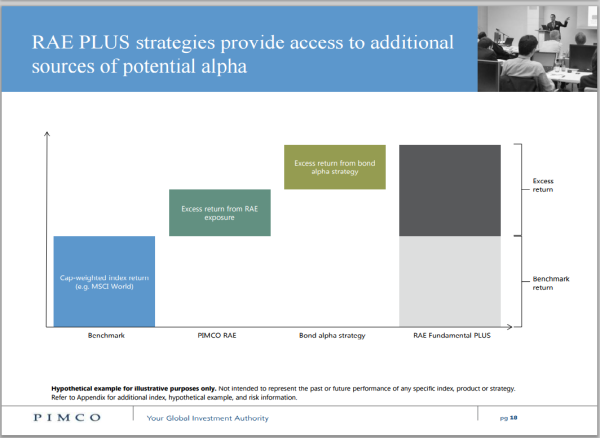

While we believed further screening to focus on quality by reducing volatility should reduce downside risk, we were actually quite surprised that Pimco had already partnered with Research Affiliates to develop a sophisticated approach to investing in the fundamental indexes that also reduces risk. This approach, before screening for quality, attempts to capture additional potential excess return using low-risk swaps that allow them to retain cash to invest in fixed income. In short, they strive to get two sources of excess return: first from the higher return of the fundamental index and second from the higher return of bonds.

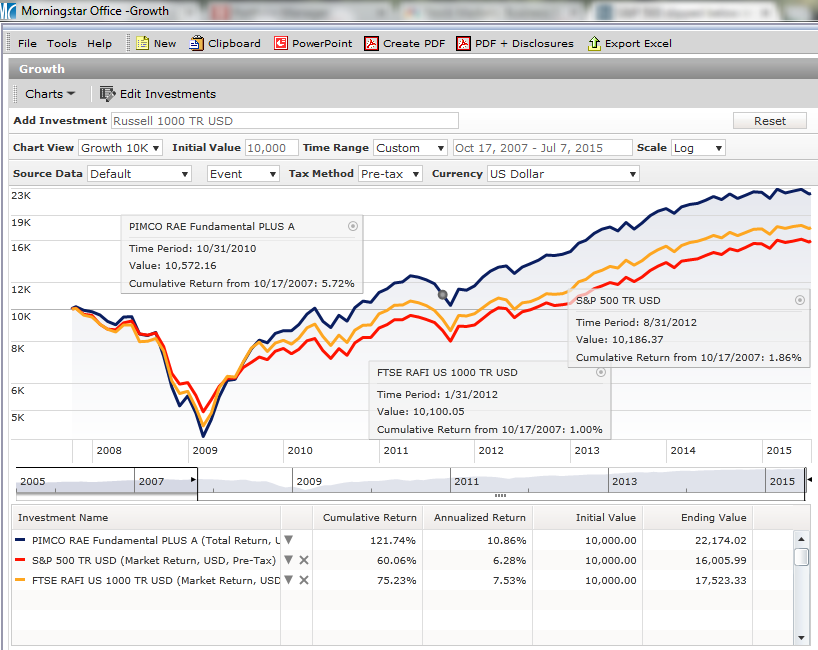

Pimco has had great success with this strategy, returning over 4% p.a. more than the index in its RAE Fundamental Plus fund replicating the US Research Affiliates fundamental index. The chart below shows the excess return the strategy generated not only on the S&P 500 index but also the FTSE RAFI US 1000 index which the fund replicates. The return boxes illustrate the approximate time each investment showed a positive return assuming perfectly bad timing before the last crisis, i.e. assuming an investor put his money to work at exactly the wrong time.

What we found most striking of this analysis was the quick recovery the Pimco fund experienced, bounding back to above positive by late 2010, a little over 3 years after the crash of 2007. In contrast, it took the fundamental index (FTSE RAFI) over four years and the market cap weighted S&P almost five. We were surprised that this fundamental PLUS overlay created a framework for lower risk before even screening for low volatility!

While this was a very useful insight, the fundamental research by academics such as Professors Bruce Greenwald and Robert Novy-Marx clearly illustrate that a quality component leads to excess return and reduced risk.

With this work in mind, Research Affiliates (RAFI) created indexes that add this quality component by further filtering the fundamental index by low volatility in order to identify the top 15% of its constituents according to low price beta, dividend, cash flow, earnings, and low debt. Since their construction over ten years ago, RAFI fundamental low volatility index strategies have added substantial value versus the market cap weighted indexes. In addition to higher returns, they have also shown substantially lower risk. While we hate to grossly generalize, based on the performance of these indexes in the US, International developed, and International Emerging markets, we believe an additional return of 2% p.a. may be captured over the long run and a risk reduction of 25%. This, especially in context of their historical investment “ulcers,” makes them interesting.

PIMCO has rights for distribution of these low volatility indexes. While we cannot plan on getting 4% p.a. more than the indexes, through the combination of excess return from fundamental and bond alpha we believe they will have lower downside risk and fit our standards for investing. Furthermore, we believe this approach is enduring and not subject to finding an excellent stock picker. The problem with stock pickers is that their success is their own undoing as the assets they manage burgeon.

To listen to our last webinar on fundamental indexing please go here: https://www.fuzemeeting.com/replay_meeting/cd837093/7349290

Integrating this into our Investment Process

Based on this new learning, we plan on increasingly making use of these fundamental indexing strategies to gain access to select markets. This does not mean we will be abandoning the managers we so carefully selected, particularly those that show the prudence of closing to new investors before becoming too unwieldy to manage risk and return going forward. IVA and Grandeur Peaks are examples such managers. Fundamental indexing is just another arrow in our quiver and a perfect supplement to the US stock strategies.

While we acknowledge the possibility that interest rates will rise, the consensus among those we respect is that they will likely stay relatively low for a while. And because “the problem with the future is that it is uncertain,” to quote Jean Marie Eveillard, we will continue to make prudent choices intended to reduce downside risk where possible but capture returns over a full market cycle always considering each clients’ unique goals.

Written by Ken Moore

Ken’s focus is on investment strategy, research and analysis as well as financial planning strategy. Ken plays the lead role of our team identifying investments that fit the philosophy of the Global View approach. He is a strict adherent to Margin of Safety investment principles and has a strong belief in the power of business cycles. On a personal note, Ken was born in 1964 in Lexington Virginia, has been married since 1991. Immediately before locating to Greenville in 1997, Ken lived in New York City.

Popular posts

-

How to Calculate Your Break-Even Age June 21, 2021

How to Calculate Your Break-Even Age June 21, 2021 -

2025 Year-End Tax Planning Checklist November 21, 2025

2025 Year-End Tax Planning Checklist November 21, 2025 -

.jpg) Roth Conversions: When They Make Sense and What You Should Consider January 07, 2026

Roth Conversions: When They Make Sense and What You Should Consider January 07, 2026 -

One Big Beautiful Bill Act: Key Tax Changes You Should Know November 26, 2025

One Big Beautiful Bill Act: Key Tax Changes You Should Know November 26, 2025