Executive Summary:

While listening to market forecasts may be entertaining we are convinced that only fundamentals matter to long-term performance and that fundamentals are bound to return to the markets.

- While the last several years have been excellent for US stock market indexes like the S&P 500 (until this year) we believe this is a price momentum move spurred by $4 trillion in money printing.

- Just like the periods going into 2000 and 2007 when price momentum strategies fared well but subsequently suffered 5 year down periods, we know that fundamentally sound strategies will once again inevitably outperform because fundamentals drive long-term stock performance.

- The disparities in valuation that currently exist are more analogous to 2000 (where some areas of the world and stocks in the US were undervalued) than to 2007 (when most stocks in the world were overvalued) further supporting our thesis.

- We now offer low cost, tax efficient stock strategies designed to be substantially lower risk than the broad market indexes but to still capture the long-term returns.

Recent Stock Market Performance has Left Value-based Strategies Behind

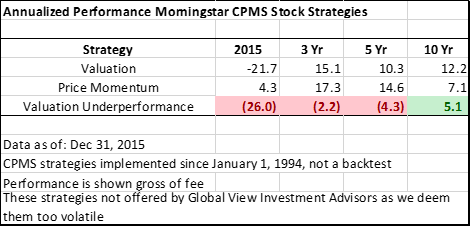

The past several years have been a very difficult time for disciplined fundamental investors. Nearly $4 trillion in quantitative easing created a tailwind for US stock market indexes. While some cheap stocks participated at first, many cheap stocks have recently gotten much cheaper. To illustrate this, the Valuation strategy, a quantitative stock strategy run by Morningstar since 1994 was until recently by far the best long run performer. This strategy selects stocks based on low valuation (price to earnings and cash flow). However, while Morningstar’s Price Momentum strategy has beaten the Valuation strategy by over 25% over the last year, the Valuation strategy has won on a ten year basis and even recently fares well since inception in 1994 despite that recent 25% performance gap, largely benefiting for the run from 1995-2000.

The Price Momentum strategy selects stocks based on recent price appreciation. Because stock market indexes are reconstituted annually based on how well prices have moved because these are also price momentum strategies. In other words, there is no fundamental reason for the prices to rise. They only rise because investors continue to bid up their prices. As soon as investor sentiment changes the prices plummet. The prices of stocks in fundamentally-based strategies like Valuation (and strategies we pursue for our clients) go up because they are cheap and because the market eventually realizes this.

Index Strategies are Risky because Fundamentals Matter

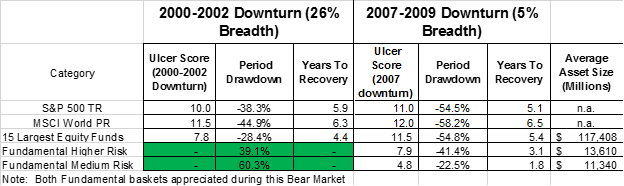

Long-standing clients know that market indexes are risky.

The chart above illustrates the true risk of market cap weighted indexes. It also underscores our thesis that fundamentally based investment strategies are more resilient as they may fall less and recover more quickly. These same strategies can do relatively very poorly over shorter 2-3 year time horizons but have historically rebounded well when the inevitable overvaluation is corrected. We calculate an investments ulcer calculate based on the amount of the short-term loss and the duration of recovery back to the original market peak investment value. Our investment thesis is now and will always be that more fundamentally sound investments will have a higher return and lower risk than price momentum based market indexes! This is a very important insight because many investors have the bulk of their net worth in 401k plans that are dominated by market capitalization weighted indexes or close index funds.

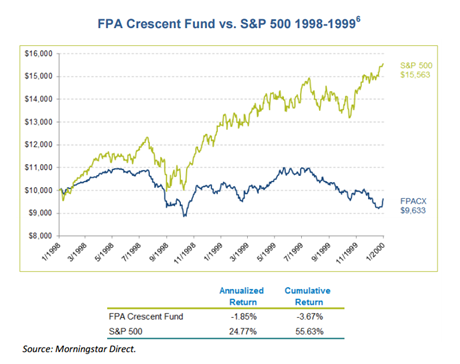

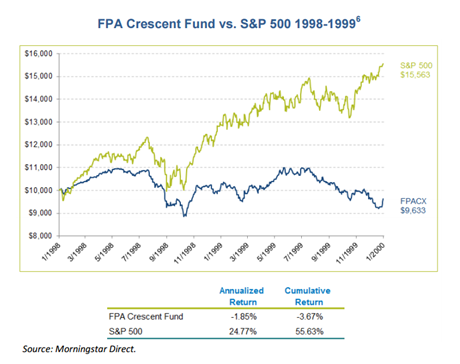

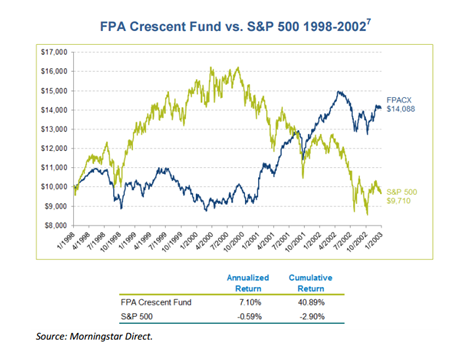

Since this cycle played out before, it bodes well for our clients going forward. To illustrate this as one of many examples the FPA Crescent fund suffered going into the dot-com bubble, losing nearly 4% during a time the S&P 500 rose over 50% from 1998-1999.

However, when investor sentiment changed from positive to negative on technology, media and telecommunications stocks plummeted when investors began looking again at fundamentals like sales, earnings and book value. This caused the companies FPA Crescent fund owned to rise substantially from 2000-2002 so that over the entire period from 1998 through the end of 2002 the FPA Crescent fund was up 41% while the S&P was down 3%.

Stock Portfolios Intended to Deliver Long-Term Market Performance with lower risk

We recently did a webinar for clients entitled Investing in Fundamentals with a MOAT to highlight our stock portfolios. Click here to listen to the recorded webinar, about 45 minutes in duration.

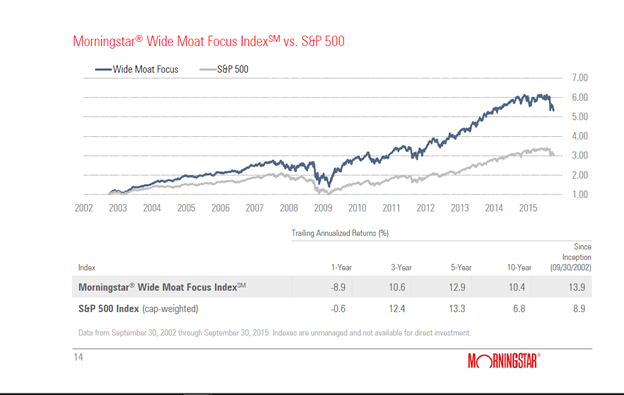

In addition to the substantial research performed by investment companies like GMO and Research Affiliates, and Professor Robert Novy-Marx which clearly illustrates that companies with superior fundamentals outperform companies with poorer fundamentals particularly in the areas of quality, valuation and growth, our portfolios draw on Morningstar’s moat methodology. Morningstar runs an index owning 20 wide moat stocks. This index is rebalanced quarterly into the 20 stocks that have a wide moat which sell at their deepest discount to intrinsic value. Results of this index are overwhelmingly positive as shown below.

Interestingly, like other valuation based strategies, this index lags substantially on a one year basis but does incredibly well over the long run and during periods of crisis by recovering very quickly.

We use Morningstar’s work to build our own portfolios with the intention of reducing risk and creating low turnover tax efficient, low trading cost portfolios. Global View stock portfolios were designed with the intention to deliver market-like returns over the long term but to have lower entry risk and risk of permanent loss of capital, especially in light of current valuations. The portfolios will own mainly US stocks and are quantitative strategies that select the top 10% of stocks covered by Morningstar that meet our fundamental criteria of valuation, quality, and growth. They are supplemented by Morningstar analysis and only buy companies that have a wide or narrow moat. There are two basic portfolios both offered in a more diversified or focused manner.

Great Businesses is designed to be the lowest risk portfolio. This portfolio owns only companies that have a wide moat meaning each company is a great business which is expected to have a sustainable competitive advantage allowing the company to earn outsized profits for a period of over twenty years. Portfolio holdings include IBM, Oneok, Magellan Midstream Partners and Philip Morris International. Most investors are familiar with the products and services these companies offer. The portfolio currently has a yield of 3.4%.

The other portfolio is called Margin of Safety Value. This portfolio may own wide moat or narrow moat companies. Narrow moat companies are expected to have a sustainable competitive advantage that allows them to earn outsized profits for over ten years. These are likely to sometimes be smaller companies that sell at better valuations. There is some overlap between these two, i.e. Margin of Safety Value will own the most attractive Great Businesses but will also own companies like Viacom, Waddell and Reed, Seagate Technology and Las Vegas Sands. This portfolio is more likely to underperform the broad market indexes at times in the hope to perform substantially better over the long run.

These strategies are an excellent complement to existing investments and are especially attractive for clients with sizeable investments outside of retirement accounts where tax efficiency is imperative.

Written by Ken Moore

Ken’s focus is on investment strategy, research and analysis as well as financial planning strategy. Ken plays the lead role of our team identifying investments that fit the philosophy of the Global View approach. He is a strict adherent to Margin of Safety investment principles and has a strong belief in the power of business cycles. On a personal note, Ken was born in 1964 in Lexington Virginia, has been married since 1991. Immediately before locating to Greenville in 1997, Ken lived in New York City.

Popular posts

-

How to Calculate Your Break-Even Age June 21, 2021

How to Calculate Your Break-Even Age June 21, 2021 -

2025 Year-End Tax Planning Checklist November 21, 2025

2025 Year-End Tax Planning Checklist November 21, 2025 -

.jpg) Roth Conversions: When They Make Sense and What You Should Consider January 07, 2026

Roth Conversions: When They Make Sense and What You Should Consider January 07, 2026 -

One Big Beautiful Bill Act: Key Tax Changes You Should Know November 26, 2025

One Big Beautiful Bill Act: Key Tax Changes You Should Know November 26, 2025