In my last blog post, we looked at 4 ways COVID-19 is affecting people’s retirement plans and what to do to get back on track. But what if you planned to retire this year? Is retiring still an option?

Finding a financial advisor for retirement is key. Then you can discuss these 4 scenarios:

1. Retire as Planned

Review your retirement savings, pensions and income-generating assets with your financial advisor to determine whether you still have enough to cover your family’s monthly spending if you retire as originally planned.

Individuals over 65 spend roughly $4,000 per month on average, or $48,000 per year. If you can maintain this amount of spending during your retirement years, you may be on the right track. Of course, every family is different and the cost of living varies by state, but this can be a helpful starting point.

Your lifestyle before retirement is a big determinant of your spending needs. Of course, you’ll have to factor in elements such as inflation, healthcare costs and any plans you had in retirement such as traveling or relocating.

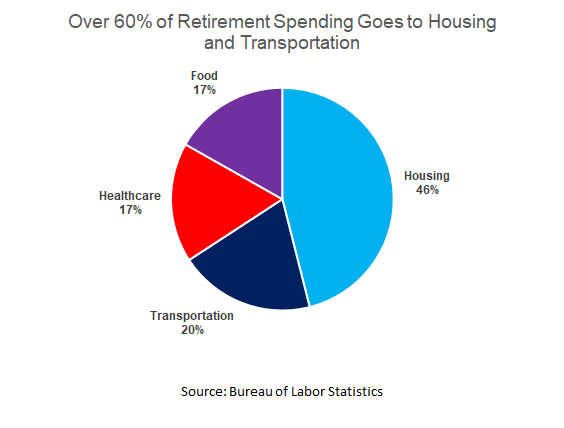

Your retirement plan should cover the vast majority of your expenses before relying on Social Security. Your biggest expenses might be housing and healthcare, with food and transportation competing for the number three spot. Be sure to fully include these costs in your retirement spending budget or reduce their outstanding balances as much as possible before you retire.

You and your family are fortunate if your retirement plans haven’t changed due to the Coronavirus. Just be sure that your plan is tailor-made to your monthly spending needs and lifestyle.

At Global View, we specialize in retirement planning and helping clients transition into this next phase in life. We also specialize in Social Security analysis. In fact, Global View Paraplanner Amanda Baize and I recently achieved the designation of Registered Social Security Analyst with the National Association of Registered Social Security Analysists. Making the wrong decision on how and when to take your Social Security benefits can cost a person thousands of dollars.

If you’re in the process of finding a financial advisor for retirement, you need help calculating your retirement income or you are ready for a second opinion, contact me directly to schedule a time to talk.

2. Push Your Retirement Date Back

If the pandemic has changed your situation or otherwise made you rethink your retirement plans, pushing your retirement date a year or more may be an effective solution. The economy lost more than 30 million jobs from COVID-19, so it’s understandable if you feel more comfortable working a bit longer and retiring later.

As mentioned earlier, retirees spend about $48,000 on average per year. So, postponing your retirement just two years can yield an extra $96,000 or more in extra income. This also gives you a chance to put your money in tax-advantaged retirement accounts a little big longer, reduce healthcare costs, pay-off bad debt and keep your Social Security benefits intact.

This decision can also result in more healthcare coverage.

If you’re covered by an employer-sponsored healthcare plan, you can better secure your healthcare coverage with a lower cost. Healthcare is a significant expense in retirement and it increases annually, likely costing more as you age.

More than one-third of Medicare beneficiaries spent at least 20 percent of their income on out-of-pocket health care costs in 2013, and that’s projected to increase to 42 percent by 2030. Working slightly longer can cut your healthcare costs and give you more savings going forward.

Pushing your retirement date a few years can also provide a bigger Social Security cushion.

In most situations, the longer you wait to take Social Security, the bigger the payment you’ll receive up to a certain point. It’s helpful to view Social Security as a supplement to your retirement income, and not the core.

Unfortunately, 47 percent of people plan to rely on Social Security as their primary retirement income. But according to the Social Security Administration, the average benefit for retired workers is $1,461 per month, or $17,532 a year, which is not enough to cover the spending of the average retiree.

While you’re eligible to receive your benefits as early as age 62, taking your Social Security benefits at 70 instead can increase the benefits you receive by more than 70 percent. This can be a significant boost to your retirement income.

Again, reach out to myself or Amanda to discuss your Social Security benefits in more detail.

Pushing back your retirement date can also give you a chance to review your financial plan and make any necessary tweaks with much more clarity. There is nothing wrong with working a little longer to improve your retirement lifestyle. Look at it as more time to save, pay-off debt and maximize your financial potential.

3. Retire and Work Part-Time

The midpoint between postponing retirement and continuing to work can also be an appealing idea.

Deciding to split your time between work and retirement, you can still experience the benefits of both. You can achieve more freedom to pursue hobbies, time with friends, etc., while gaining the peace of mind to generate income, reduce your debt and continue funding your family’s lifestyle.

Many individuals around their retirement age are choosing this option. Not only are workers aged 65 and older twice as likely to work part-time as younger workers, but more than 50 percent of people between 60 and 64 and 30 percent of those aged 65 to 69 were working at least part-time in 2017.

The boom and bust cycles and lingering economic uncertainty is driving many retirees to become more flexible during their Golden Years. There are still enjoyable jobs that retirees can pursue, which can take the pressure off of investments and preserve your Social Security benefits.

4. Retire and Alter Your Lifestyle

If you conclude that you’d prefer to retire and no longer work, you can try to make the most of your retirement assets by adjusting your lifestyle accordingly. There are a few important items to keep in mind.

Budget Accurately

It’s extremely important that you accurately account for all of your spending and taper your budget to match your mix of savings withdrawals as well as income from Social Security and other sources. Spending on certain non-essential items may need to be reduced, if not eliminated.

Finding a financial advisor for retirement can be very helpful, as a financial advisor can form a financial plan based on your actual account balances and run future projections of how your balances will be affected by spending, market gains and other variables.

Stay on One Accord with Your Spouse

Lifestyle changes aren’t necessarily easy. They become even more difficult if they aren’t properly communicated. It’s important to have a transparent conversation with your spouse about your collective financial picture and what altering your lifestyle might look like upon retirement.

This could be downsizing your home, relocating or dramatically altering your spending habits. Having a clear idea of your financial priorities will help ensure that you and your family’s needs are consistently met.

Do What Works for You and Your Family

Like your fingerprint, your financial situation is unique. Your retirement planning should be custom-made for your situation and adaptive if necessary. A financial advisor can make this process much easier for you, in any market environment.

Whether the Coronavirus ends sooner or later than expected, what’s important is that your financial plan and retirement assets are configured to support your family’s goals and needs. Having the right plan in place will make all the difference.

Finding a financial advisor for retirement is step 1.

Written by Joe Hines

Joey's primary focus is working with clients in the goals setting and financial planning process. He has extensive experience is in helping clients facilitate the decision making process, leading them through the implementation of their financial plan and contributing to their peace of mind. This includes helping clients gain an understanding of estate planning, charitable giving, and helping them implement these plans by working closely with estate planning attorneys.

Popular posts

-

How to Calculate Your Break-Even Age June 21, 2021

How to Calculate Your Break-Even Age June 21, 2021 -

2025 Year-End Tax Planning Checklist November 21, 2025

2025 Year-End Tax Planning Checklist November 21, 2025 -

.jpg) Roth Conversions: When They Make Sense and What You Should Consider January 07, 2026

Roth Conversions: When They Make Sense and What You Should Consider January 07, 2026 -

One Big Beautiful Bill Act: Key Tax Changes You Should Know November 26, 2025

One Big Beautiful Bill Act: Key Tax Changes You Should Know November 26, 2025