Yesterday Pulitzer-prize winning author Gretchen Morgenson at the New York Times, wrote another article, New York Attorney General Subpoenas TIAA Over Sales Practices, highlighting the confusopoly at TIAA.

As we discussed earlier, the financial services industry is a confusopoly (a term coined by Dilbert cartoonist and author Scott Adams), an industry which profits from customers' confusion.

Not only has TIAA been confusing customers, but literally preying on their fears. Sources at TIAA reveal: "If they cry, they buy."

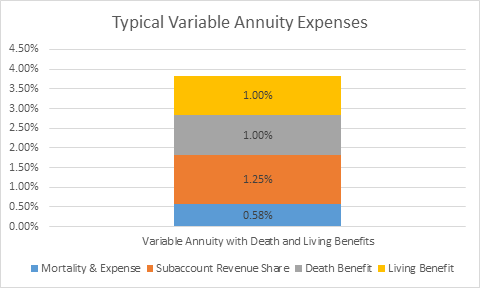

We analyzed dozens of variable annuity contracts and found variable annuities can carry an annual fee drag of 3-4% for the promise of a lifetime income stream.

Unfortunately, the lifetime income stream promised is essentially a return of capital. Are Variable Annuities Good for You, or Just the Insurance Company?

I know what you are thinking. This is wrong. You are right. It allows the company committing the deceit to profit at your expense. To placate this fear, you get sold a promise for lifetime income and don't truly understand the confusing promise until it is too late to undo.

But we already know the top management at financial services firms understand human beings are not only irrational, but actually nearly perfectly, predictably irrational (according to Nobel Laureate Daniel Kahnemann and others).

We have real-life examples of retail investors, like the poor schoolteachers and college professors at TIAA, putting their life savings into retirement plans at work, now reaching retirement and being scared into buying high-cost annuities.

When a 80 year old retired teacher client of ours heard this, having bought into the TIAA is not for profit story her entire life (things changed), she literally cried.

The worst part about this is that this is literally only the tip of the conflicts of interest iceberg!

Big banks and public insurance firms must, legally, put shareholders interest before their clients’ interest. It’s in their corporate charter. We understand these companies have to make money. Don't get me wrong, but this example is one of intentional deceipt causing a win for the company and a loss for the investor.

It’s this intentional deception that gets my goat. As a public service to educate investors, I will be spending a lot more time shining light on this confusopoly by unpacking the conflicts of interest so that you can understand it!

It's not just insurance. Remember the Wells Fargo and Bank of America scandals? Cross Selling - Is Wells Fargo Taking Advantage of Clients?

It's literally any 'fee-based' advisor.

Nearly all advisors give lip service to "fee-based." But this doesn't mean anything, because all advisors are fee-based now. It only means the advisor can charge fees or commissions, which means he can sell you annuities and other products with high hidden fees. And he will because its very profitable to do so. "Fee-based" advisors, offer conflicted advice.

Even worse, fee-only advisors can do this too. It's fashionable now for advisors to adopt the "fee-only" moniker as a bastion of virtue when in fact they can also sell products like insurance.

In the financial services confusopoly insurance is not regulated by the Securities and Exchange Commission (SEC), which means they can be "fee-only" under the SEC and also receive insurance commissions. Talk about a confusopoly!

In fact there is no authority to tell you what is fee-only, which means you need to ask some hard questions.

The two biggest enemies facing investors are their own bad behavior and the behavior of bad advisors taking advantage of their bad behavior. These two foes cause investors to leave half of their potential returns on the table.

You are probably mad about this, and you should be. Because there is something we can do to stop it.

When you understand how you are likely to behave you are less likely to behave adversely. This can be coached.

When you know how the parties you deal with are paid (when this is made transparent) they you can choose to pay them appropriately. In this situation you would never pay someone who may be working against your interests.

We use several techniques to help our clients avoid these problems.

Instead of listening to the big banks and insurance firms from Wall Street, we find sources with transparent biases (biases less confusing, easier to understand). For example, we use Morningstar for stock research instead of Wall Street firms who represent both the buy-side (investors) and the sell-side (companies).

Because Morningstar only represents buyers they don't have a direct conflict of interest. Instead their bias is indirect, because all the top financial services firms and insurance companies are also their clients. Believe me this causes a bias.

And we wouldn't think of limiting our manager (and fund) research to Morningstar. That's a story for later. I know you want to hear more but sadly you must wait.

Most advisors can exacerbate the investor return gap. Using an invalid risk assessment to understand clients’ risk causes investors to believe they have a high tolerance for risk when things have been going well and a low one when not. This can cause them to chase returns and run away from risk at exactly the wrong time.

We source our risk assessment system from Australia. That's a long way from Wall Street.

And while we use Morningstar research, we especially enjoy the view from their Canadian subsidiary, less biased by Wall Street interests.

It’s what having a global view (living years overseas and reading broadly) brings to the table.

Someone needs to translate this confusopoly so you can understand it.

As a trained linguist, I volunteer. Stay tuned. I have allies. We are unpacking this for you.

Because big banks and insurance companies can profit at your expense you should avoid playing their game. Imagine what it would be like to work with a financial advisor who tells you exactly what his conflicts of interest are so that you can know if you are playing the win/lose or win/ win game.

Ask your advisor to answer, in writing, two questions. First: Does he work as a fiduciary in all aspects of the relationship? Second: Can he receive insurance commissions?

His answer to these two questions should be: Fiduciary, yes. Insurance commissions, no. Put that in writing.

Better yet. Ask me.

For a complete list of questions, read this: Questions to Ask Your Financial Advisor

Written by Ken Moore

Ken’s focus is on investment strategy, research and analysis as well as financial planning strategy. Ken plays the lead role of our team identifying investments that fit the philosophy of the Global View approach. He is a strict adherent to Margin of Safety investment principles and has a strong belief in the power of business cycles. On a personal note, Ken was born in 1964 in Lexington Virginia, has been married since 1991. Immediately before locating to Greenville in 1997, Ken lived in New York City.

Popular posts

-

How to Calculate Your Break-Even Age June 21, 2021

How to Calculate Your Break-Even Age June 21, 2021 -

2025 Year-End Tax Planning Checklist November 21, 2025

2025 Year-End Tax Planning Checklist November 21, 2025 -

.jpg) Roth Conversions: When They Make Sense and What You Should Consider January 07, 2026

Roth Conversions: When They Make Sense and What You Should Consider January 07, 2026 -

One Big Beautiful Bill Act: Key Tax Changes You Should Know November 26, 2025

One Big Beautiful Bill Act: Key Tax Changes You Should Know November 26, 2025