Economists are warning about recession. With markets at an all-time high, unemployment at all-time lows and Americans taking home more money than any time in history, how can anyone talk about recession?

Because it’s the way economies work.

Economies slow down when they are going well and pick up when they are not. Economists know this. The stated tipping point for this economy to slow down was the fear of a large-scale trade war between the U.S. and China and unwillingness of the Federal Reserve to stop raising rates (and maybe lower them). But because economists “predicted nine of the last five recessions” (predicted five right and predicted an additional four that didn’t happen), we need to take their predictions with a grain of salt. There’s always a reason for things to slow down, but there might also be reasons for things to pick up. Right now, the main reason a slowdown or recession might be averted is the Fed’s willingness to cut rates (a pretty recent change).

Predicting the economy is above our pay grade. But looking at current fundamentals is not. Because our clients don’t want to lose money they can’t make back, it’s our job to avoid the trouble spots. I don’t have a crystal ball, but can observe:

- The U.S. Stock Market is expensive (much more expensive than international developed and emerging markets)

- High Yield Bonds are expensive

- “Safe” Bonds have low yields

- Investors fear international and emerging markets

- Investors make money by a willingness to endure short-term pain for long-term gain (but the best long-term choice is hardly ever the easiest)

So, what does this mean for investors? First, you can’t time the market. You need a good fundamental understanding of your tolerance for risk and make sure you stay allocated to that. This means you need a set portion of your wealth invested in stocks with the remainder in bonds and cash. When we are approached by investors who wonder if they can retire, we find they are taking more risk than is suitable for their risk tolerance. Even more importantly, they may be measuring the wrong things.

What’s Happening Now

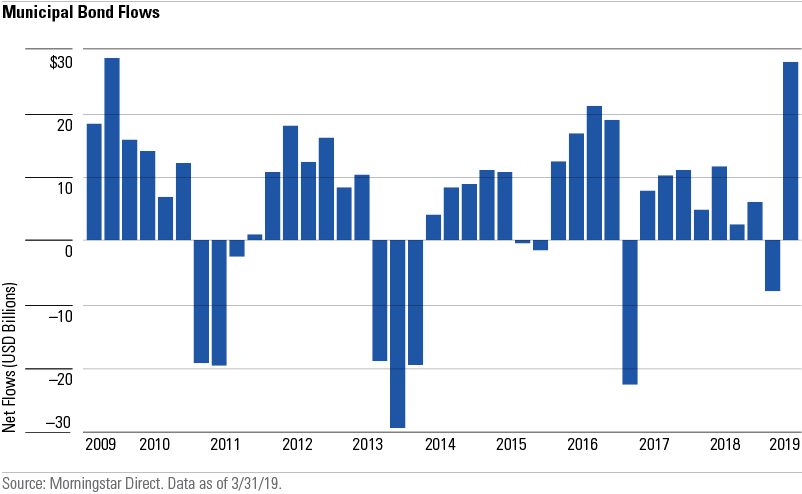

Unfortunately, the data shows investors are trying to time the market now. In the first quarter of this year alone, flows into bond funds were the highest since early 2009 when the market bottomed. But these investors are simply moving into safe bonds. They are chasing high yields, which are also overpriced.

Second, you need the right kind of exposure to risk. With more than 30,000 global companies to invest in, why should you confine yourself to the 4,000 in the U.S.? Bond markets are also diverse and much larger than stock markets. The global bond market is more than $100 trillion. More importantly, most bond investors aren’t even trying to make money! Most bond investors are required to invest in bonds of a certain type by either regulators or a misguided investment policy.

Because the world is a big place, we strive to find the best professional portfolio managers to navigate it. A couple of months ago, we invited two managers to give an overview of what they see globally. Learn more about what they said here: What World Class Investing Looks Like.

The size and diversity of the global stock and bond markets create opportunity for enterprising investors in both the U.S. and overseas. There are several disparities present today. In the U.S., smaller companies trade at a 17 percent discount to larger companies. This has made investing particularly difficult for managers focused on the best opportunities of smaller growing companies. The last time the discount was this steep was during the late 1990s during the Dot Com bubble. The good news is that this may be poised to change based on a metric followed by Leuthold Research called the Very Long-Term Momentum index.

Additionally, “value” stocks trade near their fair value, but “growth” stocks trade at 28 percent higher than their historical valuations.

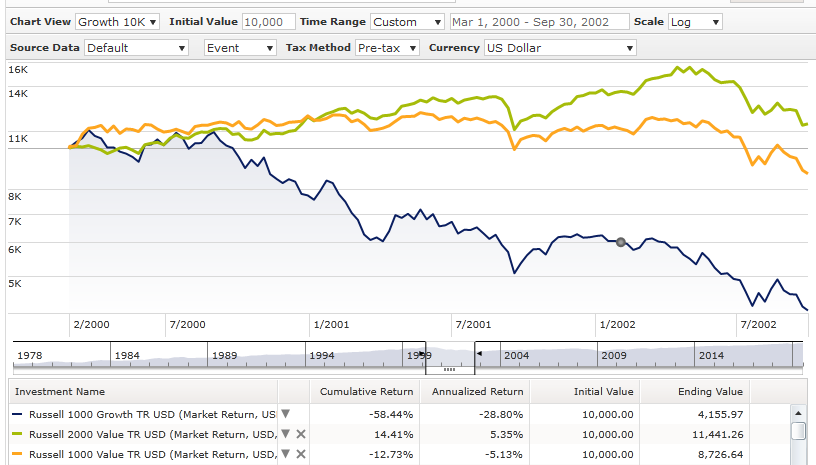

The good news here is that even when the next recession comes, it might affect portfolios similarly to the recession in the early 2000s, when small cap and value companies did well but many large growth companies did not. The chart below shows that avoiding overvalued companies, and focusing more on better valued companies, especially small companies, served investors well at that time. Specifically, from March 2000 to September 2002, large growth companies fell 58 percent, while small value companies rose 13 percent.

Index investors may find it ironic, but the best track record of any fund at the most fervent proponent of index investing, Vanguard, is the actively managed Vanguard Windsor fund under the portfolio management of John Neff. Under John Neff, the Vanguard Windsor fund, from 1964 to 1995, beat the S&P 500 index by 4 percent per year. Like all portfolio managers we admire, Neff considered value and growth characteristics of companies he selected in the fund. Among other things, he sought companies selling at low valuations and noted that the eventual rebound in the prices of these companies comes as business cycles turn and prospects of the companies improve.

After you know your risk tolerance and are looking where to allocate funds, you need an advocate to guide you in the right direction.

At Global View, we have a team of professional investment advisors and Certified Financial Planners™, an accountant and an attorney all under one roof. At it’s right here in Greenville, SC. Some on our team have been doing this for more than 20 years. We know where to start. And we know how to help you maximize your odds of achieving your goals.

There’s no cost to find out if we can help. And there may be a lot of opportunity. Contact us. Because the future of your retirement, your spouse’s retirement and your legacy to your children and the causes you care about depend on it.

Written by Ken Moore

Ken’s focus is on investment strategy, research and analysis as well as financial planning strategy. Ken plays the lead role of our team identifying investments that fit the philosophy of the Global View approach. He is a strict adherent to Margin of Safety investment principles and has a strong belief in the power of business cycles. On a personal note, Ken was born in 1964 in Lexington Virginia, has been married since 1991. Immediately before locating to Greenville in 1997, Ken lived in New York City.

Popular posts

-

How to Calculate Your Break-Even Age June 21, 2021

How to Calculate Your Break-Even Age June 21, 2021 -

2025 Year-End Tax Planning Checklist November 21, 2025

2025 Year-End Tax Planning Checklist November 21, 2025 -

.jpg) Roth Conversions: When They Make Sense and What You Should Consider January 07, 2026

Roth Conversions: When They Make Sense and What You Should Consider January 07, 2026 -

One Big Beautiful Bill Act: Key Tax Changes You Should Know November 26, 2025

One Big Beautiful Bill Act: Key Tax Changes You Should Know November 26, 2025