One of the most important decisions facing retirees is when to claim Social Security benefits. It can also be one of the most complicated.

As one of two Registered Social Security Analysts at Global View, it’s evident people are looking for a one-size-fits-all answer. But there are many elements to your financial life that need to be considered.

To help with some of the confusion, our financial advisors have created this guide: Navigating Social Security. The Global View team can also help you determine your break-even age.

What is a Social Security Break-Even Age?

Your break-even age tells you the age at which you can maximize your Social Security benefits over your expected lifetime, looking at the trade-off between age and benefit amount.

Here’s a quick breakdown:

Age 62 is the earliest age at which you can receive benefits, albeit in an amount smaller than your Primary Insurance Amount (PIA), which is the benefit you receive when you reach your full retirement age.

Every year you delay your claim beyond age 62, the amount of your annual benefit increases. Delaying your benefit beyond your full retirement age results in 8 percent per-year increases until you reach age 70.

In other words, if you claim benefits earlier, you’ll receive a smaller annual benefit, but you may receive your payments for more years. Conversely, delaying your claim increases your annual benefit (up to 132 percent of your PIA), but you might collect for fewer years.

Your break-even age is the age at which the cumulative benefits you’d collect over your expected lifetime when filing early equals the cumulative amount you would collect if you waited to file. It’s dependent on several factors, including your benefit amount, your taxes, your job plans, any spousal or survivor benefits (if applicable) and inflation.

Knowing and understanding your break-even age can help you decide the best time to claim your benefits. While you could try to noodle the answer with a spreadsheet, the financial advisors and Registered Social Security Analysts at Global View can do it for you. By inputting important information based your specific situation, our team can help you see the difference between taking your benefits at different times, ultimately helping you determine the right time to start taking Social Security benefits based upon your unique financial situation.

Looking at Different Scenarios

The beauty of finding your break-even age is to help you discover the optimal age to claim your Social Security benefits.

For example, suppose your full retirement age is 66 and your monthly benefits are estimated as the following:

- Monthly benefit at age 62: $1,200

- Monthly benefit at age 66: $1,700

- Monthly benefit at age 70: $2,200

How long would it take for the benefits claimed at age 62 to equal those claimed at age 70?

- Benefits begun at age 66 versus those begun at age 62: Break-even age is 75.

- Benefits begun at age 70 versus those begun at age 62: Break-even age is 79.

- Benefits begun at age 70 versus those begun at age 66: Break-even age is 83.

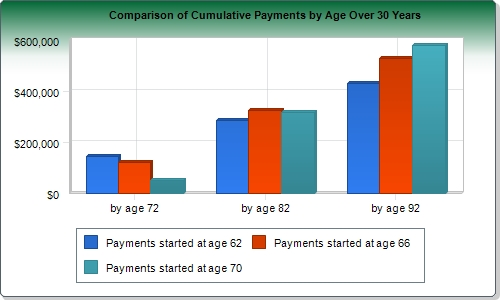

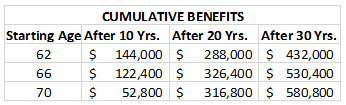

You can also view your cumulative benefits 10, 20 and 30 years after reaching the minimum claiming age of 62.

These are the cumulative benefits based upon starting age:

To give these results meaning, it’s important to understand your lifetime expectancy. Read our recent blog post: How Long Will Your Retirement Be? A Longevity Calculator.

In the example above, if you expected to live beyond age 75, you’d earn more cumulative benefits by delaying your benefits claim until your full retirement age (in this case, age 66). If your life expectancy exceeded age 79, you would come out ahead by waiting until age 70.

Furthermore, if you have it on good authority that you’ll live to age 100, you’ll draw the greatest cumulative benefits by waiting until age 70.

Caveats

While your break-even age is powerful information, keep in mind that it’s also hypothetical. Several factors can impact the benefits you’ll actually receive, including:

- Your health status and life expectancy

- Your actual lifetime

- The annual cost-of-living adjustments you’ll be receiving

- Changes to the rate of inflation

- The amount of tax (if any) you’ll have to pay on your benefits

- Your job plans

Spousal and Survivor Benefits

Your break-even age also omits the impact of spousal and survivor benefits.

You may be able to collect spousal benefits based on your spouse’s earnings record until you claim your personal benefits. You can claim a percentage of your spouse’s PIA, ranging from 32.5 to 50 percent, depending on your age when you file the spousal claim.

To qualify to collect spousal benefits, your spouse must already be collecting their personal benefit. You’ll receive the greater of your personal and spousal benefits.

If at least one spouse was born before Jan. 1, 1954, you may be eligible for a restricted application, where you can claim spousal benefits without regard to whether your spouse has filed a claim.

Survivor benefits may be available to spouses and ex-spouses of deceased benefits recipients. You can take these as early as age 60.

For more on how spousal benefits work, read our recent blog posts:

Social Security Strategies for Married Couples

Social Security and Divorce – What Many People Don’t Know

The Bottom Line

As you consider your retirement planning options, remember to look at the big picture. Do you expect your health to change? What are your work plans before and after filing your claim? Is inflation something you should worry about?

The answers to each of these questions could impact your Social Security benefits and their taxability.

Working with a financial advisor who is familiar with the ins and outs of Social Security benefits can help ensure you get the maximum benefit available to you. Other than a 12-month reset button, in which you have to pay all benefits you have received back, the decision about when to start claiming Social Security cannot be undone. Avoiding a mistake can mean the difference between a comfortable retirement and a stressful one. Don’t be afraid to ask for help.

If you’re currently looking for a financial advisor in Greenville, SC, let’s talk. Global View is a fee-only, fiduciary financial advisory firm headquartered in Greenville, SC that serves investors nationwide. Our mission is to provide truly independent, conflict-free advice and complete wealth management services, so you can protect and maximize the wealth you’ve built.

Get the ball rolling in the right direction!

Written by Erin Milner

Erin works as a paraplanner alongside our Advisors in managing client relationships and special financial planning needs, including retirement transition, education, and estate planning. Erin began working in the financial advisory business upon graduating from the University of Georgia with a BS in Financial Planning in 2015. She competed in the National Financial Planning Student Challenge in 2014. Erin is a member of the Financial Planning Association. She volunteers at Habitat for Humanity as a Financial Assessor.

Popular posts

-

How to Calculate Your Break-Even Age June 21, 2021

-

2025 Year-End Tax Planning Checklist November 21, 2025

2025 Year-End Tax Planning Checklist November 21, 2025 -

.jpg) Roth Conversions: When They Make Sense and What You Should Consider January 07, 2026

Roth Conversions: When They Make Sense and What You Should Consider January 07, 2026 -

One Big Beautiful Bill Act: Key Tax Changes You Should Know November 26, 2025

One Big Beautiful Bill Act: Key Tax Changes You Should Know November 26, 2025