{kind=link}

Despite recent market volatility and concerns over European debt contagion, it is important to remember the strategy our managers pursue, which is to avoid, at all costs, the risk of permanent loss of capital. Unfortunately, capitalizing on volatility and avoiding it are generally mutually exclusive. For example, during the worst years of the Great Depression, the market fell substantially, but had largely recovered within two years after adjusting for inflation. Our managers are taking prudent actions to reduce downside volatility where appropriate and continue to find opportunities for long-term return in this continuing difficult economic environment. At this point, they generally hold high cash balances, high quality equities and often some gold.

We rely heavily on our managers for their market outlook, but are not agnostic to general economic conditions. You may remember that we pointed out to our clients that we expected a recession in January of 2008 and took some actions in advance to reduce volatility by introducing short-term volatility control managers to client portfolios. Since then we have begun monitoring economic fundamentals more closely and will apprise our clients of anything warranting an alteration to asset allocations. At the moment, we do not expect a double dip recession in the US. More importantly, our managers have a very strong fear of inflation at some point over the next several years. Failure to own the right assets could easily result in a substantial loss of purchasing power. For this reason, we believe the Margin of Safety Investment Strategy is the best course of action to assure long-term purchasing power.

Contents:

• Historical Market Perspective: comparing inflation adjusted stock returns during the 1930s with the 00s shows that the returns during the 00s were worse than the 1930s!

• Corrections and Time Horizon: corrections often do not turn into bear markets and when they do they often bounce back in short order

• Investment Flows: Investors moved out of stocks thru March of 2009 and never really got back in, instead they invested in bonds. Given the abysmal performance of most investors in relation to the returns of investments, this should be a cautionary tale on chasing bond returns.

• Market Outlook: the line of least resistance for the S&P 500 is to rise substantially back close to pre-crash levels before another major downturn resumes; however we expect high volatility for some time and other scenarios are also possible

• Manager Commentary: Our managers believe the future holds slower economic growth and have positioned their portfolios accordingly. They are very fearful of inflation in the long term

Historical Market Perspective – last ten years versus 1930s:

Many people will be surprised to know that the last ten years in the market had worse returns than the 1930s:

• January 1 1930 – December 31, 1939: +1% p.a.

• January 1 2000 – December 31, 2009: -1% p.a.

Below is an excerpt from Grant’s Interest Rate Observer for June 11, 2010:

“In the ten years to December 31, 2009, the S&P 500 fell by 24%, without regard for reinvested dividends. In the decade of the 1930s, it fell by 42%, also without counting the dividends. But dividends in the 1930s were substantial enough, if reinvested, to deliver a 1% annual return. The meager dividend payout of the 00’s have delivered a 1% annual loss.”

If stocks suffered worse returns during the last ten years than they returned during the Great Depression (after adjusting for inflation), then why should an investor believe the next ten years will be worse? Further, if we accept the very high likelihood of inflation over the last ten years, what is the best strategy to get through the next ten years?

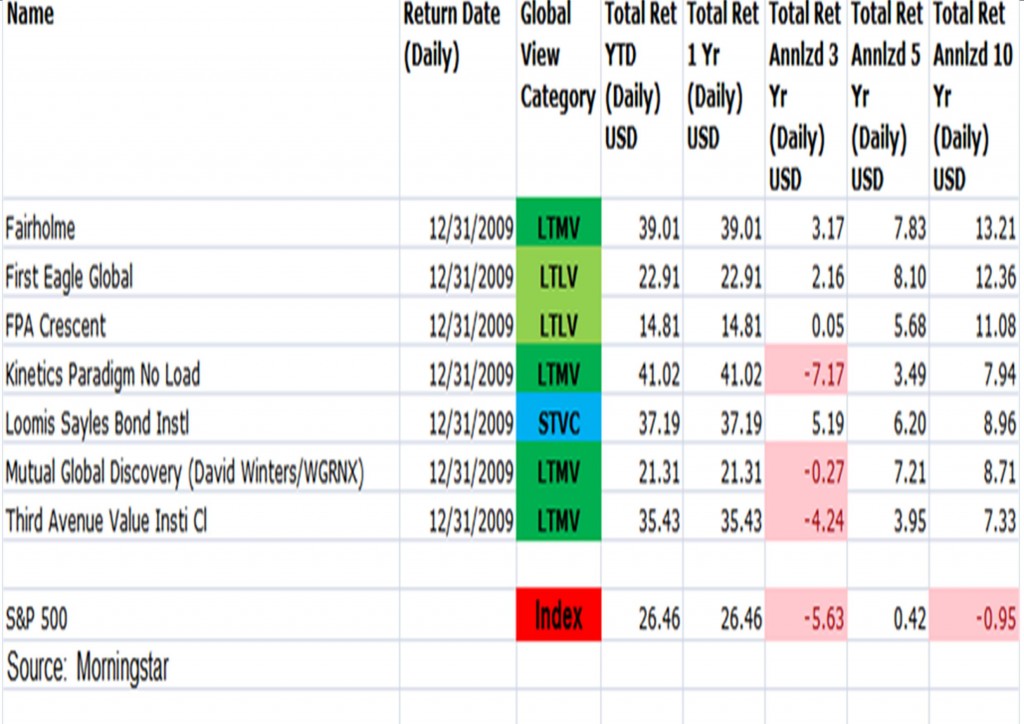

To put this in further perspective, we put together a chart describing how noted Margin of Safety Investment managers performed during the last ten years.

We believe the S&P 500 may experience low real returns for the next 10 years. We also believe that the managers we use, who focus first on capital preservation, are the best way to produce positive real returns (after inflation) than any other strategy. While the past is no guarantee of future results, we believe the MOS process is designed to thrive in a volatile low return environment because our managers will be afforded many buying opportunities.

Corrections and Time Horizon

Market Volatility returned during much of the second quarter, and world markets have experienced a substantial correction. This makes investors wonder if a bear market has resumed. Despite concerns over the economy, European debt, and the oil spill, it is important to remember how our managers find opportunities. Our managers identify and buy strong companies selling at a discount to their intrinsic value based on in-depth fundamental analysis. In this turbulent economy and difficult macroeconomic environment, these managers are more prepared for another downturn and are more focused on buying companies that are financially strong and that will survive another deep recession. Said another way, our managers are first and foremost seeking to avoid the risk of permanent loss of capital. A permanent loss occurs when a company goes into bankruptcy, or has their ability to generate profits become permanently impaired. To reiterate, avoiding a permanent loss of capital is completely different than avoiding a market correction which temporarily reduces the prices of companies you own, and consequently, the daily values of your portfolio. Ultimately, our goal for you is to attain the annualized returns you need over the next 10 years, 20 years, and longer that your money will be invested, and not attempt to avoid every correction that appears long the way. If we could do that we would because it would reduce our earnings volatility as well.

Example of the Temporary Nature of extreme Drops – A Cautionary Tale to Avoid Overreacting to Losses

During the worst years of the Great Depression, from June 30, 1931 to June 30, 1932, the market index fell in price by 67%. One year later, on June 30, 1933, the market had rebounded to within 20% of the 1931 nominal high price. However, since this two year period was characterized by a deflating dollar, as the purchasing power of a dollar increased while prices fell, the real value of the index was only 2% below peak by June 30, 1933. We feel this is relevant because talking heads point to the “losses” that were suffered during these two years, the worst two years of the Great Depression, thereby underscoring the undeniable pain of this experience. These same talking heads fail to mention the temporary nature of that very scary drop in market prices for investors who remained invested. In inflation adjusted terms, from the greatest drop, the market had almost completely recovered only one year after the low point of the great depression. The periods that preceded and followed this two year period were also quite volatile, and we are not trying to trivialize this. We simply hope to illustrate that the investing crowd, when driven by fear, can send prices up and down very rapidly and often irrationally. These sharp price moves create a lot of fear but investors with a long-term perspective consistent with the long investment time horizon of their assets should avoid trying to predict or minimize volatility that is inevitable and extremely difficult to time.

The chart below, courtesy of Leuthold Weeden Capital Management, illustrates how often corrections have occurred that did NOT turn into bear markets. Many investors are fearful that we have entered another bear market. That is not yet the case and may not turn out to be the case.

We came across a video illustrating time orientation. People are either past focused, present focused, or future focused. A focus on the future requires TRUST, whether trust in a higher being, trust in the markets, or a trust in the goodness of people to honor contracts.

To put this into the context of investing, we ask our clients to trust in the Margin of Safety strategy to work over reasonable time horizons. You may find this video entertaining and insightful.

LINK: Video on the Secret Powers of Time

Market Outlook

In his quarterly letter, Jeremy Grantham of GMO, outlined 3 scenarios for stock market returns over the next couple of years. He believes there is a 50% chance that there are no real market shocks and that the stock market rises to pre-crash levels by October of 2011 (S&P to 1550) because policy will be pursued to re-lever the economy in the hopes of political incumbents gaining re-election. However, he believes there is a 30% chance that, even with a sustained economic recovery that the market falls back to historic valuations (around 900 on the S&P); this possibility seems remote now. He believes there is a 20% chance that poor economic data or some other crash, such as the events currently being experienced in Europe, cause another market crash (for the S&P 500 to potentially fall to a new low again, say to 500).

{kind=link}

If we weigh the odds of this, we can calculate an expected value of the S&P 500 of around 1175. Based on this, were we invested in the S&P 500 index, we would see limited upside and substantial downside. But our clients are not invested in the index, thru our managers you are invested in securities around the world that have a margin of safety. These strategies have worked very well thru history and we believe they will continue to do so!

We rely heavily on our managers for their market outlook. Bruce Berkowitz has made a big bet on financial firms that he avoided like the plague before the crisis. The largest positions in the Fairholme fund include Citibank, Bank of America, AIG and Regions Financial. His reasons for doing so are that we are “in the second inning of a nine inning ballgame”, suggesting economic recovery or at least an end to the crisis, which combined with low interest rates, is a good environment for financials to perform. On the other hand, our Long-Term Less Volatile spokespersons like Steve Romick of FPA, Jean Marie Eveillard of First Eagle, and Charles DeVaulx of IVA feel there are significant economic headwinds to economic growth and that it is more prudent to be risk averse than risk taking, i.e. to hold some cash and gold and very high quality companies.

We are not agnostic to economic conditions, therefore monitor closely respected and unbiased strategists and economists who have a proven track record of highlighting potential problems but who are not always bullish or bearish. One serious headwind facing economic growth in developed nations is the debt that has been accrued at the household, company, and government level. McKinsey conducted a study showing that, after a financial crisis (like the one we just had) is experienced, a deleveraging cycle has to take place before economic growth resumes at normal historical rates.

LINK: Mckinsey report on Deleveraging

The US government has done everything it can do to prevent market forces from correcting excess leverage, which would have been corrected had defaults of the larger financial institutions occurred. Had this happened, the recession would have been steeper but the problems would be behind us. Since it did not, it we face reduced economic growth or another recession before this imbalance can be corrected. Problems in Europe are worse.

You may remember that we pointed out to our clients that we expected a recession in January of 2008 and took some actions in advance to reduce volatility. Since then, we have begun monitoring these more closely and will apprise our clients if we decide to alter asset allocations. At the moment, we do not expect a double dip recession in the US in the near future.

Investment Flows:

The chart below shows the cumulative cash flow into and out of Bond Funds and Stock Funds between 10/31/2007 and 5/31/2010. The data is compiled by the Investment Company Institute. Beginning in September of 2007, retail investors were withdrawing money from both Stock and Bond funds at a, historically, very high rate.

In March of 2009 (market low), investors began to move money back into Bond Funds (again at a historically high rate). However, investors (and particularly retail investors) still have not returned to Stock funds, as you can see on the referenced chart. The S&P 500 prices rallied up 80% off of the March 2009 low, however many retail investors bailed out and did not reinvest; thus they did not participate in the appreciation. Said another way, many retail investors locked in some or all of their losses by exiting their Stock Funds and have yet to reinvest. This is an argument supporting the view that many investors have capitulated. For those investors considering buying bonds the question is whether they should follow the crowd, who has such an abysmal track record?

Manager Updates

Short-Term Volatility Control Managers

Hussman

Dan Hussman has been and remains extremely risk averse. In his last weekly report, he shows that the ECRI leading index has moved negative, and while this is not yet sufficient to show the US economy might be falling into recession yet, he is concerned that it may in the near future.

LINK: Hussman Weekly Commentary

Nakoma Total Return

Dan Pickett is skeptical of the economic recovery which he believes is strong but slowing. The fund currently has a net long exposure of 3%, which is slightly less than in recent months.

LINK: Nakoma Quarterly Letter

Loomis Sayles Bond

The Loomis Sayles team believes the US and non-Japan Asia may be the engines of global growth. They believe increased investment by businesses and higher exports may lead a sustained expansion and, while the consumer has showed some signs of recovery, consumers lack the desire and ability to drive the recovery. Overall, their view is that the recovery is likely to be sustained and that the situation in Greece and Europe is likely to be a temporary setback.

LINK: Loomis Sayles Bond Market Review

Dan Fuss

Dan Fuss was interviewed recently. He believes that businesses and consumers have learned to live lean. “the Trauma is over, but this is not a sharp, broad-based recovery in inventories.” Since 2007, the economy experienced two recessions, one in inventories and the other in the credit markets. He thinks US consumers will be down for several years, but not a decade, and that demographic trends depict a 1957-1963 economic picture where we first had a recession, then a recovery, then a recession.

LINK: Dan Fuss Interview in FA March 2010

Nuveen Muni High Yield

John Miller runs the Nuveen Muni High Yield Municipal bond fund. Historically the fund has been less than 50% correlated to equities, treasuries, and corporate high yield and much less cyclical than corporate bonds due to the public purpose which is involved. Moreover, default rates have been substantially less, from 1986 to 2009; the cumulative average default rate was 6.3% (substantially lower than corporate bonds). Yielding 7.0% (end of March), the represents a taxable equivalent yield of 10.7% for investors in the 35% tax bracket. The high yield municipal bond market, which has recovered substantially since the end of 2008, remains at 2002 levels (substantially elevated from historical average).

We are monitoring this position closely for a deterioration; should we notice this, we will likely reallocate.

LINK: Nuveen Municipal Bond Focus Q1 2010

Long-Term Less Volatile Managers

First Eagle Global

Value investing legend Jean-Marie Eveillard believes the unfortunate reality is that, in the long-term and on a relative basis, the west is declining and the east is rising. Moreover, the question is not whether we have a recovery but whether it will be sustained. He sees three possibilities for the economic recovery:

1. Authorities lever up the system to facilitate recovery

2. Recovery peters out and we suffer Japanese style economic stagnation (which he does not believe will happen in US or in Europe)

3. We are no longer in an economic landscape of the post WWII period, but that we are in a new, undefined era. The unprecedented steps taken but the government with budget deficits, the unprecedented steps taken by the Federal Reserve including zero interest rates and ballooning of balance sheet may (or may not) lead to unintended consequences such as high inflation and suspicion to government debt.

On the problem of the deficit, Jean Marie thinks:

1. If economic growth occurs, tax revenues flow in and problem is solved

2. But … he thinks we are in a new era … unintended consequences; he did not elaborate on this. Based on earlier comments, we suspect he means a possible debauchment of the US Dollar resulting in very high inflation

Jean Marie does not have great confidence that the CPI reflects the actual inflation occurring.

LINK: Bloomberg Interview with Jean Marie Eveillard April 2010

LINK: Smartmoney on First Eagle Global

International Value Advisors

On a conference call March 31, Portfolio Managers Charles de Vaulx and Chuck DeLardemelle discuss their investment objective and the current market. Their funds have two objectives: 1. To be resilient in down markets short-term and 2. To do well against equity benchmarks longer term. Their objective is not simply to protect and preserve capital, but to preserve WEALTH. Governments and central bankers have a tendency to debase currencies, therefore protecting wealth means protecting capital in inflation adjusted terms.

While clearly the quick money has already been made, there are many opportunities around the world.

LINK: IVA conference call transcript March 2010

LINK: IVA in Barrons May 17, 2010

LINK: Factsheet

Wintergreen Fund

In this interview, David Winters talks about his outlook. He believes the world will “re-inflate” and that problems will be solved, but that you have to own the right companies in order to capitalize on this. In the short-run, more debt will be issued and companies will be restructured, but that things will work out over time, because “at some point the world is going to get better.”

The trend is for countries to debauch their currencies and in this environment it is important to own companies that can increase earnings!

LINK: Ticker Interview of David Winters May 2010

LINK: Bloomberg Interview of David Winters May 2010 (part 1)

LINK: Bloomberg Interview of David Winters May 2010 (part 2)

FPA Crescent Fund

Steve Romick tells Morningstar, in these interviews, that it has become more difficult to find good value opportunities. The opportunities they find are more in larger cap stocks. He is concerned about the Federal debt and is not sure what the effect of pulling back stimulus will have on the economy. He believes growth over the next 5 years will be lumpy. They like larger companies and overseas companies more than smaller domestic companies.

LINK: Morningstar interview of Steve Romick May 2010 (note, pause the second interview so you won’t hear both simultaneously)

Long-Term More Volatile Managers

Fairholme Fund

Bruce Berkowitz is making a bullish call on financials and the US economy. Recently, he bought big stakes in AIG, Goldman Sachs, Bank of America, and Citigroup and is the largest shareholder in Regions Financial Corp and CIT. Bruce believes we are in the second inning of a nine inning baseball game and believes that as the economy continues to recover, financials can sustain a rally reminiscent of their run in the 1990s when they rose sevenfold. Bruce’s philosophy is to put his investments through his own stress test and try to “kill the company” to see what might disrupt cash flow. On bad debt, he explains the appeal of these banks in a metaphor: the pig and the python.

For a time, the pig overwhelms the python. Eventually, the python digests the pig, the bad loans shrink, and the bank makes new loans. The bottom line: a diminished drag from past problems and growing earnings.

LINK: Bloomberg interview of Bruce Berkowtiz May 2010

LINK: Barrons Interview of Bruce Berkowitz May 2010

Third Avenue International Value

In a recent conference call with Amit Wadhwhaney, Amit expressed his discomfort in Europe/ Greece, and like our other managers had a hedge against Euro depreciation. During the rally, Amit raised some cash and felt the crisis in Europe is giving him an opportunity to put some of this to work. We look forward to learning where he is finding these values.

LINK: Quarterly Factsheet

Kinetics Paradigm

Peter Doyle, Chief Investment Strategist of Kinetics funds has a different view than our other managers. He believes volatility will fall because company balance sheets have become much stronger, i.e. non financial companies in the S&P 500 have over $1 trillion in cash, representing about 11% of their balance sheets. He also believes that P/E multiples will expand due to the very low interest rates now and expected for some time. The Paradigm fund beat the S&P 500 every year since inception except for 2008. Peter believes this underperformance was an anomaly because the performance was driven by something other than fundamentals. Moreover, he feels the outlook for current holdings is excellent.

LINK: Conference Call 4/20/2010

Other MOS Managers (Funds We Don’t Own)

Longleaf Partners

Longleaf is an investment advisory firm with an excellent long-term track record that experienced substantial downside volatility in 2008, only to recover strongly in 2009. Mason Hawkins, Chairman and CEO, said the following:

“We find that many investors currently have little interest in hearing about our company valuations, P/V rations, the great businesses we own, or the terrific management with whom we have partnered. The lack of interest in our fundamental research corresponds with ongoing macro concerns. Many believe that another show will drop from government intervention, monetary and fiscal policy mismanagement, a second leg to the recession, or some combination of these. Didn’t 2008 show that such negative macro scenarios will overwhelm our appraisals and our “margin of safety?”

Their answer, paraphrased:

• Macro predictions are adequately discounted

• Our core holdings have already survived potential negative macros scenarios and can increase prices in an inflationary scenario

• Dread scenarios could help our holdings – government intervention may help and weak capital markets will help

If you have any questions please contact us. Thank you for your continued patronage.

Popular posts

-

How to Calculate Your Break-Even Age June 21, 2021

How to Calculate Your Break-Even Age June 21, 2021 -

2025 Year-End Tax Planning Checklist November 21, 2025

2025 Year-End Tax Planning Checklist November 21, 2025 -

.jpg) Roth Conversions: When They Make Sense and What You Should Consider January 07, 2026

Roth Conversions: When They Make Sense and What You Should Consider January 07, 2026 -

One Big Beautiful Bill Act: Key Tax Changes You Should Know November 26, 2025

One Big Beautiful Bill Act: Key Tax Changes You Should Know November 26, 2025