Update on Asset Allocation and Portfolio Rebalancing for Professionals and Other Friends

7/07/2009

Dear Professionals and Other Friends,

Periodically, and at least annually, we rebalance client accounts consistent with their goals and investment time horizon. This rebalancing considers each client’s comfort with volatility, transaction costs, and tax impact. For those clients who do not have Retirement Income Accounts, we are setting these up and modifying existing accounts where appropriate.

We have rebalanced some accounts and will be rebalancing others periodically. Below is a brief description of our mission to clients, an update on the current market outlook, a description of our valuation based asset allocation methodology and rationale as well as how we select managers, categorize managers into buckets and some new manager commentary. As always we appreciate your support and welcome new referrals.

Our Mission

As your independent investment advisor, we believe our clients deserve:

- Legal Fiduciary – we work in our clients’ interests first

- Robust Investment Strategy – The Margin of Safety Strategy has worked since the Great Depression to deliver good returns over shorter time horizons than relevant indexes

- Comfort with What is Happening – we know you are a human and may be your own worst enemy if not prevented from making human mistakes

- Meaningful Relationship – we direct most of our energy to helping our clients achieve their goals

Economic/ Market Outlook Update:

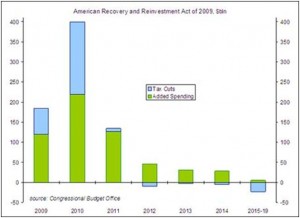

We are not in the business of making short-term market predictions. Nonetheless, we can somewhat safely conclude that the rise in stock prices over the last couple of months has occurred primarily due to efforts made by the Federal Reserve and not due to Fiscal policy. The picture below, obtained from Congressional Budget Office data, illustrates the effect of “stimulus” on the economy thus far. Bottom line, little stimulus has yet been enacted (according to the Christian Science Monitor less than 5% of the stimulus funds had been spent as of early June).

Moreover, while the rate of economic descent has slowed and global economies may be turning around, the Global Economy is by no means out of the woods. The topic of discussion, even among more bearish economists has turned away from Great Depression and toward recovery but anemic growth. We believe this is a likely scenario and have thus reduced our fair value of the S&P 500 to 950 from 1000. While we believe global economic growth will be positive, it is likely to be low in the United States over the next several years, and growth prospects outside of the United States, and particularly in Asia, are far greater.

Valuation-based Asset Allocation:

A key element of being Comfortable with What is Happening, is knowing that we are taking actions in an attempt to improve your risk adjusted performance. We also believe this will make the Investment Strategy more Robust. Note that this does NOT mean we will necessarily be making frequent changes.

By dividing long-term investments into three Buckets and weighting these Buckets depending on the relative value of the overall market, we strive to gain the benefit of the margin of safety approach and simultaneously reduce overall portfolio volatility. During periods of extreme undervaluation, we overweight our most volatile bucket (Long-Term More Volatile) and during periods of extreme overvaluation we overweight the least volatile bucket (Short-Term Volatility Control). During periods of fair valuation and moderate overvaluation, we will generally have more in the Long-Term Less Volatile bucket.

Currently we believe the fair value of the S&P 500 is 950. At its current level of 920, this is close to fair value. It is important to note that the market usually trades in a range between fair value and 40% overvalued, trading below that range only during periods of extreme uncertainty. Moreover, the fair value will rise over time. Our allocations reflect the fact that the market is currently in the fair value range. In this range, the greatest allocations for Moderate and Moderately Aggressive risk tolerances are in the Long-Term Less Volatile Investment bucket.

We envision reallocations on an annual basis; however, should the price of the overall market fall to extreme undervaluation (below 620) or extreme overvaluation (above 1280) we will reallocate. Other events that would cause us to reallocate include termination of a manager or hiring of a new manager.

Rationale:

While nothing is more important than manager selection and due diligence, we believe the risk/ reward enhancement of managers is different at differing valuation levels. All investors fear loss when faced with volatility and may even capitulate, locking in losses permanently. This is the greatest tragedy. The graph below shows a description of how well market indexes have fared as opposed to how well investors have fared according to Dalbar. Interestingly, investors in allocation funds fared no better than those in equity funds.

Explanation of Allocation Buckets:

As we create our allocation models, we use three broad categories of managers who are employed to meet different objectives. They are:

- Short-Term Volatility Control (STVC) – Our objective for these managers is to control volatility over an 18-month time period by generating returns higher than cash and government bonds. Therefore, we would not normally expect to experience losses over 18-month periods. We feel it would be extremely unlikely for these managers to experience losses over 3 year periods. We also expect these funds to perform more poorly than the stock market benchmarks during bull markets. The Retirement Income Account is comprised entirely of managers from this bucket and cash.

- Long-Term Less Volatile (LTLV) – Our objective for these managers is to control volatility over 3 year time horizons by generating positive returns and to beat the returns of relevant stock benchmarks such as the S&P 500 or the MSCI World index over the long run. We expect these funds to have less volatility during extreme down and up markets but to perform well as long as valuation disparities exist.

- Long-Term More Volatile (LTMV) – Our objective for these managers is to generate high returns over periods of more than 5 years and to substantially beat relevant stock benchmarks such as the S&P 500 or the MSCI World index over the long run. We expect these funds to have similar volatility to benchmarks during extreme down and up markets and to substantially outperform relevant stock benchmarks such as the S&P 500 or MSCI World index as long as valuation disparities exist.

Manager Selection Criteria:

The biggest mistake investors make is choosing funds by looking only at historical performance, particularly recent historical performance. We have a systematic process for quantitatively ranking managers according to multiple criteria for both return potential and volatility control. Historical performance is only one criterion used and is relevant only over long time horizons.

Criteria considered for Long-Term Return Potential (Long-Term More Volatile and Long-Term Less Volatile) include:

- Margin of Safety Investment Objective (stated and implied by action)

- Shareholder First Attitude

- Asset Size of Overall Fund Assets

- Flexibility

- Own Cooking Eaten

- Manager’s Track Record (as opposed to fund track record)

- Implied Return Objective

Criteria considered for Short-Term Volatility Control include:

- Degree of Diversification

- Overall Downside Risk (Magnitude and Odds)

- Ability to Hedge

- Flexibility

- Stability of Strategy

- Ownership Concentration (in single issues)

Categorization by Investment Bucket

For those managers who rank high on Long-Term Return Potential, we divide these into investment Buckets according to the following criteria:

- Degree of Diversification

- Downside Magnitude (95% and 99% Confidence)

- Downside Probability (below reasonable goal targets)

More volatile managers are placed in the Long-Term More Volatile Bucket; less volatile ones in the Long-Term Less Volatile Bucket.

Manager Commentary:

We have received positive feedback from clients on access to manager interviews. Outstanding Investor Digest attempts to bring the most important ideas and insights of money managers with the best long-term records in the business. Below are two interviews from its latest edition. The first interview is with Bruce Berkowitz of the Fairholme Fund, the second with David Winters of the Wintergreen Fund. They both give great insight into what they currently own and why they own it, as well as a glimpse into their professional belief system.

Outstanding Investor Digest interview with Bruce Berkowitz March 17,2009

Outstanding Investor Digest interview with Dave Winters March 17, 2009

While we hold CNBC in somewhat lower esteem, below is an interview with Matthew McClennan of First Eagle. In this interview, he explains how their fund is a modern day investment Fort Knox, preferring Japanese companies with solid balance sheets and no debt. Below are three links to commentary featuring this fund. He also voices his fears that US growth prospects are meager, favoring investments outside of the US.

First Eagle Global CNBC interview May 28, 2009

Robert Gardiner, late of the Wasatch Microcap fund, launched a new fund in October of last year, the Wasatch Global Opportunities. Below is a description of how he and Robert Blake approach the investment process:

Wasatch Global Opportunities May 5, 2009

Conclusion:

In an upcoming newsletter, we intend to explore more deeply the benefit of active managers versus passive strategies. Recent evidence suggests that even commonly held mutual funds have substantially outperformed market indexes. In the meantime, please contact us if you have any questions (including on Cash for Clunkers, green rebates, etc.) and we hope you enjoy a pleasant summer.

Popular posts

-

How to Calculate Your Break-Even Age June 21, 2021

How to Calculate Your Break-Even Age June 21, 2021 -

2025 Year-End Tax Planning Checklist November 21, 2025

2025 Year-End Tax Planning Checklist November 21, 2025 -

.jpg) Roth Conversions: When They Make Sense and What You Should Consider January 07, 2026

Roth Conversions: When They Make Sense and What You Should Consider January 07, 2026 -

One Big Beautiful Bill Act: Key Tax Changes You Should Know November 26, 2025

One Big Beautiful Bill Act: Key Tax Changes You Should Know November 26, 2025