Executive Summary

The second quarter was a difficult climate for investors. Until June, major stock indexes were generally doing well; however, June was a bad month. By the end of the quarter the major stock indexes had fallen. As of mid year, the S&P 500 and MSCI world index were both down nearly 12%. The only asset class that really worked was commodities. The DJ AIG Commodity index was up 27%.

As of the end of the second quarter, The Global View Investment Advisors Moderately Aggressive allocation, if invested on January 1st as of our beginning of allocation, was down 2.2% before fees. This return is hypothetical because the only way it could have been achieved is if all funds were invested on January 1st and no deposits or withdrawals were made.

Economic Uncertainty and Stagflation?

With a presidential election looming, oil prices and food prices soaring, and plenty of populist politicking, some investors are getting nervous. As of this date, the Dow Jones is now in a Bear market, as defined by having experienced a 20% decline. Moreover, there is a consensus that a US and perhaps global economic slowdown have already begun.

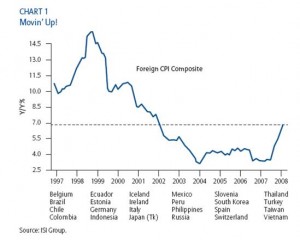

Thankfully, the bond managers we respect at Pimco and Loomis Sayles believe the worst of the credit crisis is behind us. Their greatest concern is inflation. A Morgan Stanley study shows that 50 countries around the globe have inflation at 10% or more, representing about 3 billion people; overall foreign CPI is currently about 7%.

Thankfully, the bond managers we respect at Pimco and Loomis Sayles believe the worst of the credit crisis is behind us. Their greatest concern is inflation. A Morgan Stanley study shows that 50 countries around the globe have inflation at 10% or more, representing about 3 billion people; overall foreign CPI is currently about 7%.

The consumer price index (CPI - the most commonly used indicator of inflation) in the United States is only 4.3%. This doesn’t make intuitive sense to households, who have seen a dramatic rise in gasoline and food prices.

The US Bureau of Labor Statistics (BLS) is the government agency that compiles CPI data. The CPI is intended to be a cost of living index instead of a general price index. Ironically, the largest component of the CPI is something called owner’s equivalent rent. Owner’s equivalent rent is based on housing prices and accounts for about 25% of the index. What this means is that while the inflation rate may still be relatively low, this is of little help to the average American family of four with an income of $40,000 to $60,000. They are worse off because they have lower wealth (lower house value) and higher expenses at the same time. This increase in discretionary expenses may squeeze out other spending and further slow the economy.

Consumer sentiment, as measured by the University of Michigan index has declined to 56.4, the lowest in over 20 years and back to 1980 levels. Today, oil imports represent about 3.2% of GDP, also back to 1970s and 1980s levels. However, our economy is very different than the late 70s/ early 80s. First of all, after tax profits currently represent about 8% of GDP, versus about 4.5% in 1980. Second, unemployment is about 5.5% versus about 11% in 1980. We are wise to be concerned about this, but also wise to not overreact.

No one is perfect

In his latest letter to shareholders, Marty Whitman of Third Avenue funds revealed that he made some mistakes in security selection. Marty shows how the Bear Sterns crisis was exacerbated from a short term liquidity crisis into near bankruptcy when financial institutions started a raid on Bear Sterns. While Marty did not own Bear Sterns, his funds owned other financials. The financials he purchased because he felt there was a substantial margin of safety; however, he overlooked the fact that a bear raid (for instance by bear raids) on the companies could cause a liquidity crisis and a loss of access to capital markets. The point is, like Bill Nygren with Oakmark, Marty Whitman made a mistake. None of these managers are perfect. For this reason, we question their purchases, monitor changes in management closely and make sure our clients own multiple managers.

Why we don’t make big bets on Trends

David Galland, the Managing Director of Casey Research, shows how an investor could have taken $35 in 1970 and turned it into nearly $160,000 today, representing a return of nearly 70% p.a. All you had to do was make four decisions:

- Be in gold in the 1970s

- Be in the Nikkei in the 1980s

- Be in the Nasdaq in the 1990s

- Be in Crude ever since.

All you had to do is make four bets. Hmm. What if you made these bets incorrectly? If you got into any of these indexes at the wrong time you would have exposed yourself to a serious risk of permanent loss of capital.

While we agree there very well may be a secular upswing in the demand for oil (primarily due to increased demand in China), it appears the price has gotten completely out of whack. Oil has risen from about $57 per barrel in February of 2007 to over $140 per barrel, an increase of over 145% in a little over a year! From December 2004 to December 2007, the notional value of over-the-counter commodity derivatives rose from $1 trillion to $8.4 trillion (up 740%).

The $64 million question is whether the rise in oil prices is attributable to growing demand relative to supply or increasingly to speculative bidding based on rising political risks in the Middle East.

There are several reasons we believe oil prices will fall. First, we have already seen higher oil prices result in a drop in demand in Developed nations.  For instance, demand for oil products declined by 2% for the 12 months ending in May in the United States and Japan and by 5% in Germany (www.oilmarketreport.org). While demand in developing nations (particularly China) has held steady or is rising, these nations have been subsidizing oil consumption. The Congressional Budget Office of the US estimates oil consumption in China will grow by 4.5% p.a. through 2010, about half as much as it grew 2003 and 2004. The question is for how long they can afford to do so.

For instance, demand for oil products declined by 2% for the 12 months ending in May in the United States and Japan and by 5% in Germany (www.oilmarketreport.org). While demand in developing nations (particularly China) has held steady or is rising, these nations have been subsidizing oil consumption. The Congressional Budget Office of the US estimates oil consumption in China will grow by 4.5% p.a. through 2010, about half as much as it grew 2003 and 2004. The question is for how long they can afford to do so.

Market Outlook

The subprime contagion in the US will affect global demand for goods and services and result in a slowdown. Moreover, with index values remaining at high multiples to earnings, few indexes look attractive. For this reason, we need to be invested globally and we need to own alternative investments. In 2007, the gap between world GDP growth and US GDP growth reached a 25 year high. We don’t believe, by any means, that the US is headed for an absolute decline; however developing nations have a lower base to start from and are likely to grow at higher rates than the US for many years.

Conclusions and Recommendations

There are too many variables to forecast with any certainty what will happen in the global economy.  Should we actually face a stagflationary period, it is of paramount importance that we strive to beat inflation, which may prove difficult in cash or bonds. During the period of 1972 and 1973, the S&P 500 fell by 42%, only to rise by 57% over the subsequent two year period. Similarly from 1929 to 1932 the market fell 71%, only to rise 148% from 1933 to 1936. Our managers strive to avoid this type of volatility but nothing is guaranteed.

Should we actually face a stagflationary period, it is of paramount importance that we strive to beat inflation, which may prove difficult in cash or bonds. During the period of 1972 and 1973, the S&P 500 fell by 42%, only to rise by 57% over the subsequent two year period. Similarly from 1929 to 1932 the market fell 71%, only to rise 148% from 1933 to 1936. Our managers strive to avoid this type of volatility but nothing is guaranteed.

We are continually monitoring our investments and manager’s reactions to the changing environment. First, our managers have substantial holdings outside of the US. Second, many have high cash balances. Third, new opportunities arise as prices fall. For instance, one manager has made a substantial reallocation from the energy sector to the health care sector. He believes there are a lot of 65 year old people who want to live past 100 (and are willing to pay to do so) but the prices of the stocks in the health care sector do not reflect this reality.

Upcoming Events

The next scheduled event is a class at Furman University. Investment Strategy in Retirement, begins September 8th to November 14th 9:00 a.m. to 10:30 a.m. A similar class will be repeated at the Reserve at Lake Keowee in February of 2009.

We will keep you apprised of other events as they arise and welcome the opportunity to meet with you to show you additional research we have completed, discuss changes to your plan, and address concerns.

Popular posts

-

How to Calculate Your Break-Even Age June 21, 2021

How to Calculate Your Break-Even Age June 21, 2021 -

2025 Year-End Tax Planning Checklist November 21, 2025

2025 Year-End Tax Planning Checklist November 21, 2025 -

.jpg) Roth Conversions: When They Make Sense and What You Should Consider January 07, 2026

Roth Conversions: When They Make Sense and What You Should Consider January 07, 2026 -

One Big Beautiful Bill Act: Key Tax Changes You Should Know November 26, 2025

One Big Beautiful Bill Act: Key Tax Changes You Should Know November 26, 2025